20s is the age of possibilities.

This is the critical time where your life starts to unfold.

This is when you begin to take on adult responsibilities like a job, a home, a car, a family and so on.

It is the age when the foundation for your life’s many milestones are being laid. Each of these milestones come with their own financial commitments and challenges. Your actions in tackling them can have lasting repercussions throughout your life. Therefore an efficient financial plan is necessary for you to thrive in the midst of these challenges.

Financial planning is not only about money. It is about building up resources that can help you reach your goals. It is about understanding your dreams and the life you are aiming to live.

The biggest mistake in financial planning is often not having a plan.

Here are 6 strategies that will help you navigate the world of finance in your 20s.

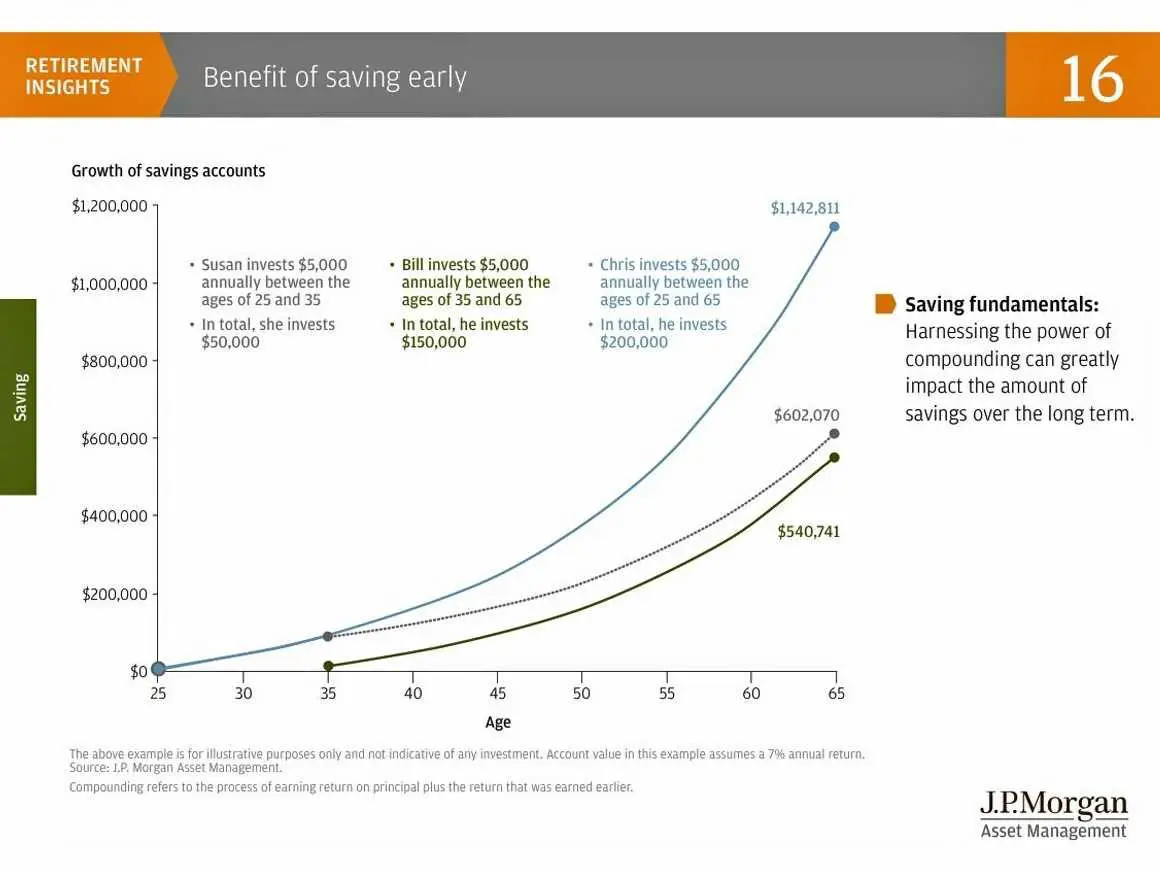

Importance of saving for compounding returns in the long-term

The worst piece of advice you will receive in your 20s is to not ‘settle’ into your career and to have adventures and take risks.

This attitude will seriously harm the financial prospects in the long run. Adults under the age of 35 - the millennials - have a savings rate of negative 2%.

29% of Americans have no emergency funds.

Less than 50% of people in their 20s have some form of retirement savings.

If you buy things you don't need, soon you will have to sell things you need.

Not keeping aside a part of your income in savings is the sure-fire road to debt and delinquency. Start as soon as you can and with as little as you can.

We often make the mistake of thinking that we have enough time to catch up or it makes more sense to save more when you are earning more. This logic is proven faulty due to compounding returns.

Thanks to compounding interest, when you start saving outweighs how much you save.

Albert Einstein called compound interest the “eighth wonder of the world”, adding: “He who understands it earns it; he who doesn’t pays it.” Compound interest is simply the interest earned on the interest.

14% of millennials have no savings at all.

As demonstrated in this chart, by investing only $50,000 over 10 years, Susan has managed to have significant savings just by starting early. Any investment can earn compound interest - even just savings.

You need not be a Wall Street wizard nor do you need to have substantial amount to start with. Save as much percentage of your income as you can spare - preferably 20% or more. The earlier you start saving, the more your buffer will be against the ups and downs of the markets.

Pro Tip - Compound the interest on your savings quarterly rather than yearly. Compound as frequently as possible to maximise the earning potential.

1. Learn how the tax system works

Taxes are complicated but they are also inevitable. Acquiring rudimentary knowledge of the tax structure on your income can help you save money and make better investment choices. Knowledge of taxes can help you budget efficiently and manage your expenditure.

A Nerd wallet survey found that, “Thirty-four percent of millennial taxpayers say they ask tax-related questions of friends or family — instead of a tax professional (27%), online sources (20%) or the IRS (9%)”. Further, “Four of five (80%) millennial taxpayers report fears related to tax preparation — such as making a mistake (22%), not getting the biggest possible refund (17%) or paying too much in taxes (13%).”

In the light of this, tax planning should be a year round activity, in which you take help from qualified professionals.

(Take this Quiz and check how updated you are on your tax knowledge.)

According to IRS in 2015, US citizens were refunded on an average $3,218. If you keep your refund amount as close to zero as possible, you could have $252 to pay your debt or invest.

While making any investment, make sure you have studied all the tax implications.

For example, some incomes earned on investments may be taxable in the same year (eg mutual funds and cash accounts). Some contributions made to an investment might be tax deferred wherein investments are sheltered from taxes as long as they remain in the account (ex 401(K)). Then there are some tax free options like Muni Bonds.

Pro Tip - If you are earning less than $62,000 p.a. use the free file technology on IRS website to file your returns for free. Get your tax refunds directly deposited into your Bank account through e filing.

2. 401(k) and retirement plan - give it a look!

Retirement seems so over the horizon, most of us don’t spare it a thought.

The study 'Retirement Savings Crisis' by National Institute on Retirement Security found that in the age group of 25-34, average retirement savings was as low as $13,000. In Wells Fargo research, it was revealed that in companies which do not automatically enrol eligible employees, only 13.45 of the millennials participated in the retirement savings plan.

Non-participation can be a major roadblock to future financial security and investment opportunity.

To avoid this, 401(K) and Roth IRA are the most viable automatic savings plan for 20 somethings to build their wealth for retirement.

401(K) is the employer sponsored retirement savings plan. Your employer will take out a percentage of your pretax income towards this account. Then the employer will match your contribution up to a predetermined percentage.

For example if your salary is $50,000 and you have a 3% match, then both you and your employer will both contribute $1500 towards your retirement account. You can increase your contribution if it’s affordable, but the employer will not pay more than that.

The employer contribution is literally free money, so max out and contribute the maximum amount you can spare. Aim to increase this periodically or whenever you get a raise.

401(K) contribution is deducted before taxes, thereby decreasing your taxable income. However, your account will be taxed at the time of withdrawal.

Roth 401(K) is another employer sponsored retirement plan wherein the contribution is made with after- tax dollars. There is no upper limit and withdrawals are tax free.

If your employer does not offer a 401(K) match, then you can opt for Roth IRA .

Roth IRA is a retirement savings option wherein your contribution is taxed at the time of deposit and withdrawals are tax free.

For example, Let us assume that you start contributing $5,000 annually to a Roth IRA account. At the age of 59, you would have $ 686,184 tax free in your account. Alternatively, in a taxable plan your account would have $470,694.

In your 20s you can take advantage of this early tax as you will be in the low tax bracket. This has income caps (< $11,700) and contribution limit (< $5,500), making it suitable for early earning years. You can even make certain withdrawals - like $10,000 to purchase your first home, without any penalty or before the age of 59.5.

Pro Tip - Your retirement savings can be significantly affected depending on whether you choose after tax Roth (K) or tax deductible 401(K). Use this Calculator to get the basic idea and plan accordingly.

3. Clear your education loan, debts and keep your credit score low

Debt is the inescapable reality for most of us. When managed well, it can be a springboard for opportunities. But if you let it linger/grow it can wreak havoc.

Two major debts we have all used are education loans and credit cards

Education Loan -

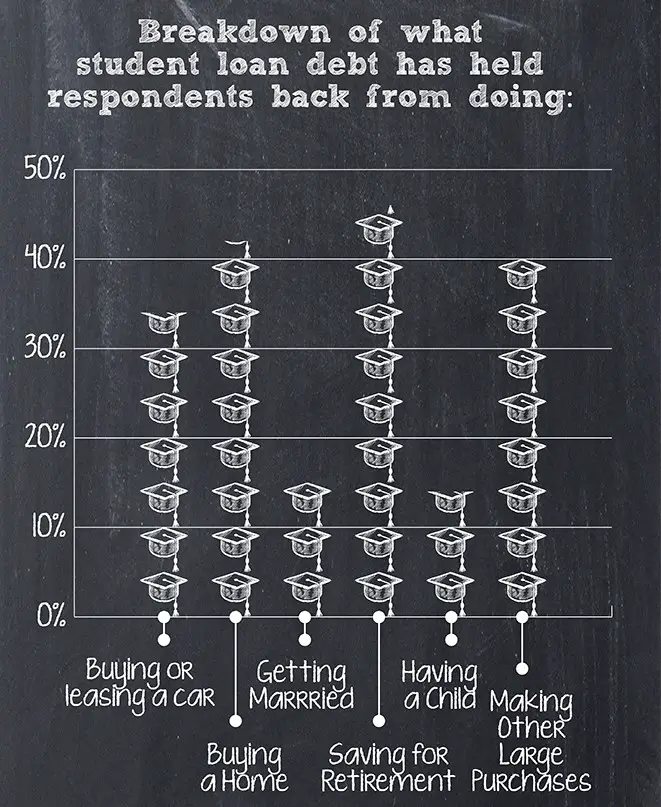

The average class of 2016 graduate owes $37,172 in student loans. 20 to 30 year olds are paying $351/month on an average towards these loans. Have you realised that, your student debt has the potential to derail your best laid plans? You are not alone.

The student debt poll by consumer credit found that, educations loans had held back people from saving for retirement (>40%) and Buying a home(>30%).

It is impossible to clear the student loan overnight. But with an optimised repayment strategy and discipline you can make inroads into it and lessen your burden.

Here are our top tips to help you with Education loans -

Select your plan carefully - prevention is better than cure. Choose the plan that best meets your ability to repay and suits your career plan.

Know exactly what you owe - Track down your loans (Federal and private). Make a list of how much you owe, at what rate and what is the minimum payment. Keep track at all times.

Pay more than your monthly minimum - This will not only reduce the principal but also the accruing interest on the outstanding amount.

Grace Period - make use of this if it’s absolutely necessary. Try to make at least interest only payments. This is crucial as accrued interest is capitalised and added to the principal even during the grace period.

Use any windfall or extra money towards repayment - This might call for sacrificing on luxuries on your part. But it is crucial to spend at least a significant part of your windfall (ex tax refunds) towards clearing your debt.

Explore Refinancing - As soon as you have landed a stable job and built up a good credit score, explore options for refinancing at a lower rate of interest. Check if you qualify for any loan forgiveness program before refinancing.

Pro tip - Remember that you are not locked into your chosen repayment plan, whenever your financial circumstances change (ex-unemployment or promotion), you can opt for a plan better suited for your situation.

Credit Card Debt-

This is the time when you will be building your credit history.

For the first time you will have a credit card connected to your own bank account and not your dads.

So, it is important to know the rules of credit card game so that you don’t end up with a mountain of debt and out of control spending habits.

Here are our top tips for using credit cards the right way -

Review your credit card statements thoroughly each month - Go through each transaction and ensure that you were charged the right amount. Check if your repayments have been properly appropriated.

Choose a card with rewards - Preferably one with cash back rewards over travel rewards like flights /hotel stays. You monthly normal spending won’t qualify for these in most of the cases.

Check the terms - Be thorough to check the terms of the card in detail before committing, Check if your card has an annual fee - this essentially means you pay to use it. Another catch is cash advances - on which interest is compounded daily.

Don’t use it as substitute for cash - Don’t get into the habit of swiping your credit card for everyday purchases like groceries and gas.

Pay more than the monthly minimum - This will help clear the debt faster and reduce the amount you owe.

Stay within 30% of your credit limit - This makes repayment manageable and helps with credit score by keeping the income to debt ratio low.

Pro Tip - Consider transferring your balance to card with lower APR score. Though it has a fee, the transfer can help you get a lower rate of interest in the long term.

Credit Score -

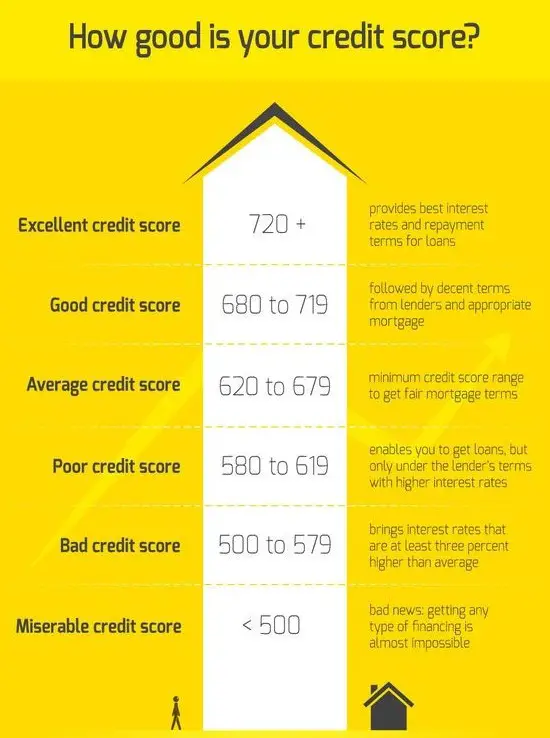

Your credit score could make or break your ability to get a mortgage, buy a car, get a credit card or get any other type of loan.

It has the critical impact on the amount of loans and at what rates you get it. As young adults, 20 somethings have opportunity and time on their side to build good credit score.

Credit score is determined by factors like - payment history, outstanding debt, and credit history, types of debts and pursuit of new credit.

Having a credit score of <680 will force you to avail loans on lender’s terms and above average rates of interest.

Here are our top tips to achieve and maintain a healthy credit score -

Make your debt repayments on time and ensure the minimum payment. Payments delayed for more than 30 days are reported to the credit bureau. Late payments stay in your history for as long as 7 years.

Don’t max out your cards or take your spending very near to the upper limits. This will raise your debt to credit ratio.

Don’t be a credit card Junkie - Don’t owe money to multiple cards, it shows that your spending is out of control. Accordingly, if you lend money get it back. Not collecting shows carelessness.

Avoid inactivity - If you don’t use your card for more than 18 months it may be closed.

Don’t be debtless - Sign up for a credit card with small limit and build repayment history with affordable payments.

Diversify your debt - Take an instalment loan (eg mortgage, auto loan) along with revolving debt (credit card).

Pro tip - Check your credit reports regularly. A Federal Trade Commission study found that 1 in every 4 American had errors in their credit reports. 4 out of 5 consumers who had their credit report corrected experienced significant change in their credit score.

4. Inculcate negotiation skills early in your career. Don't let price be your competitive difference.

The salary.com survey found that 1/5 of the employees don’t negotiate their salaries.

It is shocking, considering a person who fails to negotiate his first salary stands to lose as much as $500,000 by the time he is 50.

A whopping 44% don’t even discuss salary raise during reviews. Major factor holding them back? Fear and lack of negotiation skills.

When you are trying for a job, you are in a position of disadvantage - negotiation wise. The company and HR have huge amount of info about you and they are professional negotiators. If you walk into the negotiation room without the right arsenal, you will be ripped off.

This could undermine both your present and future earning potential.

Did you know, according to Salary.com, 55% have developed their negotiation skills by themselves?

So, it is possible for you to teach yourself to become an effective negotiator.

Here are 10 Basic strategies that can help you even the field while negotiating

Don’t settle - Not negotiating or settling for the initial figure offered is the mistake committed by most job seekers. There is always room to negotiate upwards and even a difference of couple of thousand dollars is good than nothing.

Know your value - Study the market for your skills and qualifications. Explore the current rates for similar positions in the Industry on sites like payscale, glassdoor, Career Bliss etc. Figure out the amount agreeable to you but always leave room for negotiation.

Focus on the value addition - Don’t sell yourself short. Draw attention to the qualities you possess and how they can add value to the company in terms of both money and work.

Let the Employer make the offer - Always let the employer offer the initial salary figure. Don’t reveal your present salary or the salary you expect beforehand. This will rob you of the only advantage you have.

Explore performance based incentives - Discuss the possibility of performance based incentives and set the specific, measurable parameters beforehand.

Discuss non-cash incentives - View your compensation package in totality. Discuss the non-cash perks that might bridge the gap between your expectation and your employer’s offer.

Be patient - The right time for negotiating salary is when you are deep into the process and are the last candidate standing. Asking at any point before can come across as too focused on money. By this time the company is also deeply invested in the process to walk away easily.

Don’t give on the spot acceptance - Never accept an offer the moment it is made. Take some time to evaluate your options and inform your response.

Written communication - Always conduct negotiations through email, wherein you have the record in black and white. Also ask the employer to put his final offer in writing.

Don’t be afraid to walk away - Know your bottom line and don’t settle for less than that. Be polite in your refusal but be firm about your needs.

Pro Tip - Constantly update your skills and stay relevant in your field. This will give a great boost for you negotiating position.

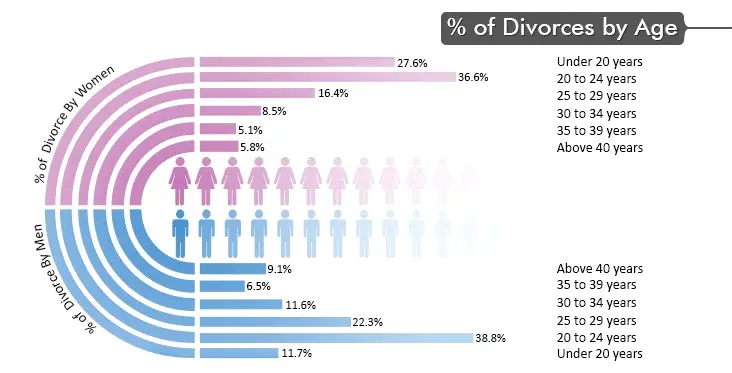

5. Bonus gyan - mind your relationship.

Marry the person you love and be ready to stay committed.

Financial planning is very important before marriage - this is relevant for twenty year olds because they will get married in an average of 5-6 years of time. Being married can leave you with significant savings as you will share expenses and budget accordingly.

Divorces leave a huge negative financial impact.

It is a $28 billion industry with average cost of $20,000 per couple. The spousal support and child support can add up over time up to 10 to 40% of your income.

No matter how amicable the divorce is, fees of two sets of legal teams can be another significant drain.

Divorce also comes with several hidden costs. An example of these is the capital gains the couple sacrifice when they liquidate investments early for division of assets. This could come with taxes and penalties.

Pro Tip - Did you know, 86% of couples who had trouble in their marriage reported that things improved over time? Go for divorce only as a last resort and not as a go to solution.

Conclusion

The first step towards financial success is realising that you are in charge.

Research and understand the implications of your financial decisions. Set realistic goals and review them periodically. Start small -have bite sized targets that can be achieved on a monthly basis.

With right approach and discipline you can build your expertise to reach your financial targets.

Are you willing to invest little time and effort in your 20s to organise your finances?